On This Day: 1995 - The UK's oldest investment banking institute, Barings Bank, collapses after a rogue securities

Quick Historical Background Founded in 1762 by Francis Baring and his brother John, Barings Bank was the oldest merchant bank in London.

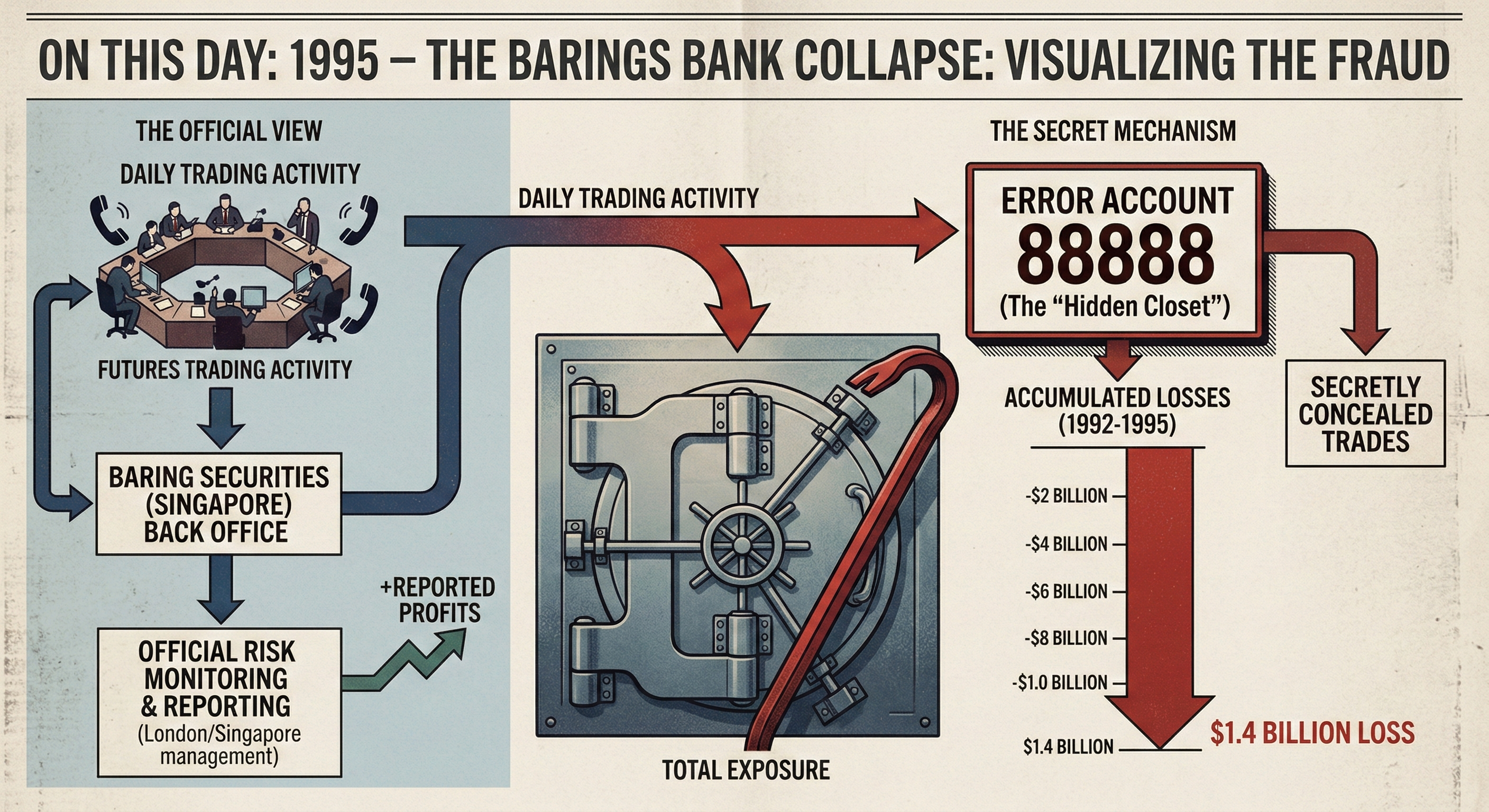

On This Day: 1995 - The UK’s oldest investment banking institute, Barings Bank, collapses after a rogue securities broker Nick Leeson loses $1.4 billion by speculating on the Singapore International Monetary Exchange using futures contracts.

1992: Nicholas Leeson, a 25-year-old derivatives clerk from Watford, is promoted to General Manager of the Futures Markets at Baring Securities (Singapore) Limited.

July 17, 1992: Error account “88888” is established to hide a clerical mistake by an inexperienced staff member; Leeson uses it to begin concealing his own unauthorized losing trades.

1993: Fictitious profits from the hidden account reach £10 million, triggering massive executive bonuses across the London headquarters and solidifying Leeson’s reputation as a “golden boy.”

January 17, 1995: A magnitude 6.9 earthquake strikes Kobe, Japan, sending the Nikkei 225 index into a tailspin and shattering Leeson’s massive “long” position.

February 23, 1995: The hole in the balance sheet reaches £827 million-exceeding the bank’s total share capital-and Leeson flees Singapore, leaving a handwritten note reading “I’m sorry.”

February 26, 1995: The Bank of England declares Barings Bank insolvent, marking the end of a 233-year-old financial titan.

Quick Historical Background

Founded in 1762 by Francis Baring and his brother John, Barings Bank was the oldest merchant bank in London. For over two centuries, it functioned as the financial backbone of the British Empire and played a pivotal role in global geopolitics. In 1803, the bank famously orchestrated the financing of the Louisiana Purchase, allowing the United States to double its land area by purchasing territory from Napoleonic France for $15 million. This level of prestige earned the institution the nickname “The Sixth Great Power” of Europe, alongside the five major nations of the era.

By the early 1990s, the bank sought to maintain its relevance in a rapidly modernizing financial world. While its traditional corporate finance and asset management arms remained conservative, its securities division became increasingly aggressive. The firm looked toward the emerging markets of Asia for growth, specifically through the Singapore International Monetary Exchange (SIMEX). This expansion required a new breed of trader-hungry, energetic, and willing to navigate the complexities of high-frequency derivatives.

Timeline of Key Moments

In 1989, Nick Leeson joined Barings as a back-office clerk, a role that gave him an intimate understanding of the bank’s settlement and reporting procedures. When he moved to Singapore in 1992, he was granted an unprecedented level of autonomy. Crucially, the bank’s management in London allowed him to serve as both the head of the trading floor and the head of the settlement office. This dual role meant that Leeson was effectively responsible for reporting on his own trades, a fundamental violation of internal banking controls that typically require “four eyes” to oversee any transaction.

By December 1992, the hidden account 88888 was already hemorrhaging money. Leeson began using futures contracts-agreements to buy or sell an asset at a predetermined price at a specified time-to speculate on the movement of the Nikkei 225 stock index. He engaged in “doubling,” a risky strategy where a trader increases their position after a loss in hopes that a market correction will recoup everything. Throughout 1994, he successfully manipulated the bank’s internal software to show massive profits while his actual losses sat in the 88888 account, invisible to the auditors in London.

In late 1994, the bank’s internal audit team expressed concerns about the lack of separation between Leeson’s front and back-office duties. However, because Leeson appeared to be generating nearly 20% of the entire firm’s profits, the senior management chose to ignore the warnings. The culture of the era prized high-yield performance over stringent risk management, and the lack of technical understanding regarding derivatives among senior executives in London left them unable to decipher the true nature of Leeson’s activities.

Turning Point

The catastrophic collapse was catalyzed not by a failure of the financial markets, but by a force of nature. On January 17, 1995, at 5:46 AM local time, the Great Hanshin earthquake devastated the Japanese city of Kobe. The disaster killed over 6,000 people and caused an immediate collapse in the Japanese stock market. Prior to the earthquake, Leeson had placed a massive bet that the Nikkei 225 would remain stable or increase in value. He believed that the Japanese economy was on a recovery path and that his “long” position would eventually pay off.

When the market plummeted following the earthquake, Leeson did not cut his losses. Instead, he intensified his gambling, buying thousands of more contracts in a desperate attempt to drive the market price back up. He was essentially betting against the collective sentiment of the global financial market with money that did not belong to him. Between January 20 and February 20, 1995, his losses spiraled from £200 million to over £800 million. By the time the bank’s management in London realized the scale of the exposure on February 24, 1995, the situation was irrecoverable.

Sources, Bias, and Debate

Historians and financial analysts continue to debate whether Nick Leeson was a “rogue trader” acting in isolation or a scapegoat for a culture of systemic negligence. The official Bank of England report, published in July 1995, heavily criticized the senior management of Barings for their failure to implement basic checks and balances. Some researchers argue that the “rogue trader” narrative serves the interests of the banking industry, as it focuses on individual criminality rather than the inherent flaws in institutional oversight.

The collapse of Barings was not merely the result of one man’s deceit; it was a systemic failure of oversight that permeated the highest levels of the London office. While Leeson’s actions were undeniably criminal, the management’s willingness to accept astronomical profits without questioning their origin suggests a culture of willful blindness. Internal auditors raised red flags in late 1994, yet these warnings were neutralized by the bank’s desire to maintain its competitive edge in the burgeoning Asian markets. This tension between risk management and the pursuit of profit remains a central theme in financial history, highlighting the dangers of allowing the front office to police itself without independent verification.

There is also a persistent debate regarding the role of SIMEX. Some critics argued that the Singaporean exchange should have noticed the massive concentration of contracts held by a single firm and intervened earlier. However, the exchange maintained that it provided all necessary data to the bank, and it was the bank’s responsibility to monitor its own exposure.

Aftermath and Follow-Through

On February 26, 1995, the Bank of England attempted to coordinate a rescue package, but the potential liabilities were so vast and uncertain that no private institution was willing to step in. The oldest merchant bank in London was sold to ING for a single pound sterling.

Nicholas Leeson was eventually arrested at Frankfurt Airport on March 2, 1995, after a week-long international manhunt. He was extradited to Singapore and sentenced to six and a half years in Changi Prison for fraud and forgery. He was released in 1999 after being diagnosed with colon cancer, from which he later recovered. The collapse led to a fundamental shift in how global banks manage operational risk. The Basel Committee on Banking Supervision subsequently introduced more rigorous capital requirement frameworks, specifically addressing “operational risk”-the risk of loss resulting from inadequate or failed internal processes, people, and systems.

The institutional pride of a 233-year-old firm vanished in a single weekend.

The legacy of the collapse remains a cautionary tale in financial education. It served as the primary catalyst for the “Middle Office” revolution, where risk management departments were given the authority to override trading desks. In the years following 1995, financial institutions worldwide invested billions into automated monitoring systems designed to detect the very patterns Leeson used to hide his losses in account 88888. Despite these advancements, the human element of greed and the psychological pressure to hide failure continue to present challenges for global financial stability.

Sources

- Barings Bank: https://wikipedia.org/wiki/Barings_Bank

- Nick Leeson: https://wikipedia.org/wiki/Nick_Leeson

- Singapore International Monetary Exchange: https://wikipedia.org/wiki/Singapore_International_Monetary_Exchange

- Futures contract: https://wikipedia.org/wiki/Futures_contract

- Bank of England Archive: “Report of the Board of Banking Supervision Inquiry into the Circumstances of the Collapse of Barings,” published July 18, 1995 (reference lookup recommended).

- Fay, S. (1996). The Collapse of Barings. Richard Cohen Books (reference lookup recommended).